Transforming Bill Pay Into An Engaging Personal Finance Tool

A little over 25 years ago, paying bills required some effort. Back then, your options were to write and mail a check, pay over the phone or pay your bank to do it for you. As the Internet grew from obscure curiosity to popular, albeit costly, obsession in the early ‘90s, banks began to offer a new, more convenient option: online bill pay. No longer would you need to write check after check; all you had to do was log on and make the payments electronically.

Granted, to enjoy this convenience at the time required spending thousands on a personal computer, and hundreds more on network equipment and service fees. Still, despite the relatively small target market, online bill pay was popular among those who could afford it. For banks, that made it a powerful tool for digital engagement and customer retention, simply because no one else could offer anything like it.

Banks soon realized that if they offered this online bill pay service for free, their customers were more likely to stick around and open a savings account, take out a home loan, seek financial planning advice, and so on. The “stickiness” that free bill pay created far outweighed the cost of the service.

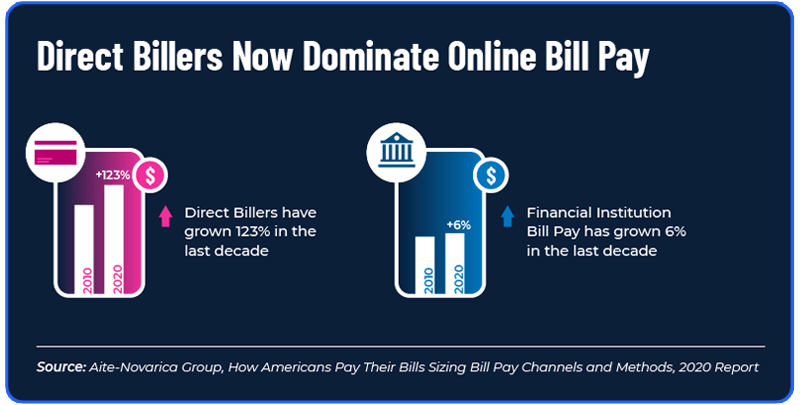

Unfortunately, for financial institutions, we’re not in the year 1995 anymore. Consumers have a number of choices in not only how they pay their bills, but also in how they deposit, move and even borrow money. Today, 76% of online bill payments are made directly at biller websites, with online payments made at direct billers growing 123% in the past decade. Meanwhile, banks’ share of online bill payments have shrunk in the past decade, from 38% down to 22%.

What’s more, a number of dynamic challenger banks and fintech startups are starting to encroach on other established bank products, displacing deposits and diminishing the importance of the checking account. Payment apps like Venmo make it easy to move money between friends, and consequently, just leave money in the app. According to the Financial Brand, some $2.2 billion just sat in users’ accounts in 2017. Health savings accounts now account for $97 billion in assets in 2021, Denevir Research estimates — doubling in just four years. Banks and Credit Unions are no longer the central hub of their financial lives. It could be, though, if you think of today’s millennial mobile user as 1995’s desktop internet user.

How Times Change

While online bank bill pay was truly a transformative technology when it was introduced a quarter-century ago, it hasn’t changed much since. Payments can take anywhere from 1 to 10 days to post, often with no assurance from the biller that the payment has been posted. By today’s standards, it’s an inconsistent system that fails to include the many payment methods consumers now rely on: debit cards, credit cards and digital wallets. If I can get a 72” big screen delivered the same day by Amazon, why is that my “electronic/digital bill pay” is still a multi-day process?

With your average consumer paying between 12 and 15 bills a month—and most of those consumers reporting feeling uncomfortable and even anxious about paying bills on time— traditional bank bill pay simply just doesn’t meet the consumer's needs anymore.

In the absence of any meaningful innovation in bank bill pay, most billers went ahead and created a better experience themselves. You can see your amount due and bill details if needed. You can pay with your favorite debit card, rewards-based credit card, or digital wallet. Most importantly, you can see your payment post in real time. It’s just a better experience.

While this might seem like all doom and gloom for banks, the good news is that the same logic from 25 years ago still applies today: Bill payment is still an opportunity to engage customers; the approach just needs to change.

The Power of Bill Center and the Instant Payment Network®

On the surface, it might seem like a herculean task to not only overcome over two decades of technological debt, but also to convince customers — who have now come to rely on their billers to make payments — to come back to bank bill pay. Though consumers’ financial lives may be headed to something more atomized and dispersed, that’s not where they want to see things headed.

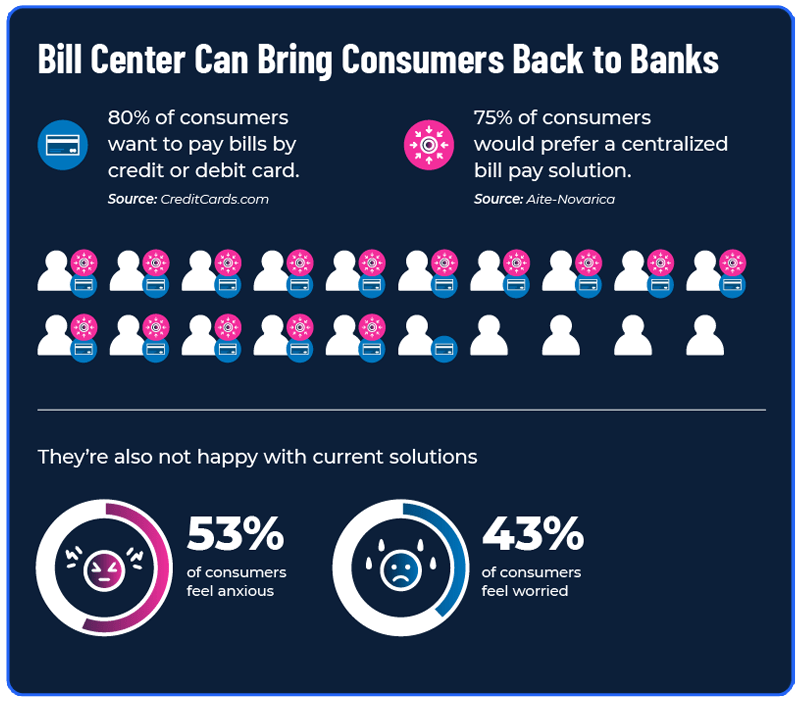

Consumers love paying their bills with credit cards because they get rewards. But if the average consumer is paying 10-15 bills each month — most of them at different biller sites — that creates a fragmented experience for consumers. This leads to consumers significantly underestimating just how much they’re paying on bills. One 2018 West Monroe survey found that consumers spend 197% more on subscriptions than they think they do.

This is why 75% of consumers would prefer a centralized bill pay solution, according to Aite Novarica, and 80% of consumers want the option to pay bills by credit or debit, according to a CreditCards.com survey.

So, what if your customer could have their cake and eat it too? It sounds cliché, sure. But really: Let’s say that you could offer your customers a single location where they could see all of their bills, subscriptions and other financial obligations. Then they could pay eligible bills with a credit card or debit card, all in one place. Do you think it would bring the convenience factor, and ultimately the stickiness and customer retention, back to bank bill pay? Do you think that giving your customers complete visibility into their current financial state would make it easier for them to manage their money? Sounds great, right? Well, you can achieve all of that — centralization, flexible payment, and increased customer engagement — with Paymentus’ Bill Center(SM), powered by The Instant Payment Network ®.

With Bill Center, your customers can centralize all of their bills, subscriptions, and other financial obligations, track due dates and cash flow, and create flexible ways to automate and schedule payments. In addition, the real power of Bill Center is that it leverages our Instant Payment Network(R), which provides connectivity to 15,000+ billers, real-time bill presentment, real-time card payments, and real-time money movement all from a single platform.

Bill Center provides your customers with a personal finance tool that empowers them with a better understanding of their financial health and simplifies money movement on their journey to financial freedom. Now that’s how you make money movement meaningful.

Bringing Meaning to Money Movement

We believe that providing the capabilities and convenience of a centralized financial hub coupled with real-time money management and movement will simplify your customers’ lives and keep you at the center of the consumer's financial universe. And, ultimately, that’s good for everyone involved.

Bill Center gives FI customers the ability to gauge their financial health in a single, easy-to-access place. It’s a win for customers, because it makes it easier for them to manage their money and focus on financial goals, whether they are borrowing, investing or saving. It’s also a win for the FI, as customers who have a solid grasp of their financials are better positioned to take advantage of other products and services the FI offers. And because customers are spending time on banks’ digital banking, FIs have more opportunities to offer more relevant products and services to them.

Beyond pure engagement metrics, Bill Center also creates an opportunity to redefine the relationship with your customers. By offering the infrastructure for consumers to build a comprehensive look at their financial health, you get a clearer picture of your customer’s spending habits. This can be used to create products and services tailored to meet their specific needs. In other words, a more engaged customer base leads to a more collaborative relationship and better services.

If you’re curious about the impact Bill Center can have for your institution by the numbers, take a look at our latest infographic, and get in touch. We’d love to help you bring meaning to money movement for your customers.